The following is an op-ed by Jay Kapoor. He has worked closely with sports media and technology companies in both operating and advisory capacities over the last five years and is currently an Associate with Techstars in New York. Prior to Techstars, he helped build MESA/Houlihan Lokey’s sector coverage in sports and live entertainment where his clients included WGT Media, FanDuel, NEP Broadcasting, Brooklyn Bowl and the Pro Bowling Association. Previously, Jay worked at the National Football League on corporate strategy, financial planning and business development initiatives for the 2012 – 2015 NFL seasons. You can reach him on Twitter @jaykapoornyc and read more of his work at JayKapoor.com.

On August 22nd, Kobe Bryant rang the opening bell at the NYSE and revealed his $100M venture capital fund, becoming another in the growing line of professional athletes to re-imagine themselves as early-stage technology investors.

With the immense amount of new wealth generated in sports over the last decade coupled with reduced barriers in the media and technology sectors, there are more exciting ways for players to lose their money than ever before.

At this point, I’m sure you’ve come across the statistic that nearly 80% of NFL athletes go broke or are financially insolvent within their first three years out of the League. Or that within five years, 60% of NBA players will go broke. Heck, they even gave The Rock an ironically named show about this.

If you’re curious, most analysis cites some combination of a (1) lack of good financial guidance (2) large entourage of hangers-on to support (3) family pressure (like disproportionately high divorce rates) and (4) ego. Yet, despite the financial struggles of once cash-flush players being a well-researched, oft-publicized and continually depressing phenomenon, it seems no one has learned their lesson.

Whereas athletes in 90’s and early 00’s were aggressively buying up real estate and striking lopsided deals to open steakhouses and novelty restaurants, the current generation of players are chasing profits in an industry with even rarer prime cuts.

Leading Lambs to Slaughter

For every Jordan’s, Ditka’s, Frazier’s, Billy Sims or Brother Jimmy’s there are 10 other failed restaurant investments by current and former professional athletes. The list of failures is as long as it is hilariously depressing, featuring the likes of:

- Rocket Ismail’s “Rock & Roll Cafe” (Hard Rock Cafe-knock off)

- Vin Baker’s “Fish House” (Make up your own joke here)

- Yao Ming’s Sushi Restaurant (But…but…he’s not Japanese?!)

- Hulk Hogan’s “Pastamania!” (I wish I was making this one up)

- Dwyane Wade’s “D. Wade Sports Grill” where he famously faced a $25M+ lawsuit a few years ago, being blamed by his business partners for its failures due to a lack of promotional appearances.

And these are among the ones that we know or care about.

Joe Theismann, who has invested in many restaurants in the D.C. area and has actually had success along the way, cautions would-be restaurateurs:

“It’s the dumbest thing anybody could do to think they could operate a restaurant as an athlete. Even if you understand the food business and have worked in a restaurant, it’s an ever-changing business that presents new challenges every day.”

Tiki Barber, who has experienced first hand the challenges of maintaining financial security post-career and now works with retired players on financial literacy, also agreed:

“…Friends and family approach athletes and say “Hey buddy, I have a great idea — let’s go start a restaurant.” It’s the worst business that athletes can get into. It feels like something they can get their hands around, and it’s really about their celebrity, but when their celebrity fades, do you still have the business?”

Restaurants are among the worst, most illiquid investments athletes can make and it takes more than star power and loyal fans to launch and maintain a restaurant, let alone turn a profit. By most accounts, a really successful one will take around two years to return its initial investment while a typical restaurant takes four to five years — if it makes it that long. By CNBC’s 2016 estimation, around 60% of new restaurants fail within the first year. And nearly 80% shutter before their fifth anniversary, including all of the ones I mentioned above.

But to me, that is actually preferable to the fate that awaits many retired-athletes turned novice venture investors.

So Much Sizzle… For Such Little Steak

Kobe Bryant’s $100 Million venture fund to investment in technology, media and data companies is perhaps the biggest of these new funds but Bryant Stibel isn’t the first time athletes have fancied themselves as investors, particularly at the seed and early stage.

Here is a preliminary list of current and retired athletes actively investing in tech and some of their notable venture investments:

Some interesting observations:

- Players above played predominantly in one of four major markets: San Francisco, New York, Los Angeles or Boston. I’m sure you can draw some causation lines from that but in the interest of getting to my point, we can table this analysis for now.

- A strong majority of the players (12 out of the 18) came from the NBA where (unlike the NFL) player contracts are guaranteed and where recently even middle of the road players are getting league-max contracts. I could only find one female athlete investing in tech and she happens to be the highest earning female athlete of all time.

- Even adjusting for my own sampling bias in the companies above, a significant number of investments made by the athletes were understandably in sports technology or digital media with an overwhelming majority being in consumer-facing tech. Current players like Chris Paul and Steph Curry more actively invested in wearable or performance-enhancing technologies more so than retired players.

- The last and most important thing is that all of these players (with the exception of Steph Curry, who will complete the trend in 2017) have received successively higher contracts and/or multi million dollar endorsement deals over their long and lucrative careers.

Honestly, it’s not these athletes that I’m really worried about. Given the amount that they are investing as a relative percentage of their total earnings and the fact that most of them partner with savvy, veteran investors to launch and manage their funds, I believe that these athletes and superstars by-and-large can afford the hits that await them.

It’s the me-too athletes that worry me.

Every time Andre Iguodala goes on stage at TechCrunch Disrupt or Peyton Manning takes a break from opening Papa John’s franchises to invest in a popular digital media company, I can’t help wonder how many players coming off the bench are saying “Yeah, I should get myself a piece of that action” — opening themselves up to risks they shouldn’t take.

Unfortunately, the odds are just not in their favor.

An Amuse-Bouche on Venture Capital and VC Math

This generation of athletes is the first to grow up with technology and the first to maximize its potential as a tool to engage with fans and each other. Tech is as much a part of their present as they hope it will be of their future. So I get the appeal. Becoming a VC is the dream of an increasing number of athletes and it feels like a perfect job for the intellectually curious tech enthusiast.

As a VC, you’re tasked with learning as much as possible about new markets and segments, meeting with the smartest people you can find and develop a unique point of view. You have the opportunity to work closely with enthusiastic entrepreneurs on their products, helping smart, determined, and audacious founders turn ideas into successes. Thanks to Twitter, Medium and tech journalism, VCs are becoming celebrities in their own right. What a great way to leverage cachet as a retired player and re-invent yourself as a savvy Silicon Valley investor – with a loyal following to-boot.

If the CEO is the coach, in the muck every day with his team trying to succeed despite the odds, the VC is the General Manager, surveying the landscape and searching for undervalued opportunities to help his coaches win.

But much in the way that only one in 30 or 32 teams can win the Finals or the Super Bowl each year, just returning a fund is really hard and making out-sized returns is even harder! Even the best ones run into trouble.

Let’s do some back of the napkin math. Assuming you have a:

- $25M seed fund

- Setting aside $15M for first checks / keeping $10M for follow-ons

- Average check-size of $0.5M for first checks / $2M for follow-ons

You can invest in 30 companies and follow-on for 5 of them. Just to get your money back i.e. return the fund, you need:

- One company (where you invested $2.5M) to return 10.0x

- Two companies to return an average of 5.0x

- And so on…

Most early-stage funds make their returns off just a handful of investments. To borrow a baseball metaphor, singles and doubles just won’t cut it. Venture investing is a game of home-runs. USV’s Fred Wilson says:

…our target batting average is “1/3, 1/3, 1/3” which means that we expect to lose our entire investment on 1/3 of our investments, we expect to get our money back (or maybe make a small return) on 1/3 of our investments, and we expect to generate the bulk of our returns on 1/3 of our investments.

Venture Capital Investing is Rarely a Medium Done Well

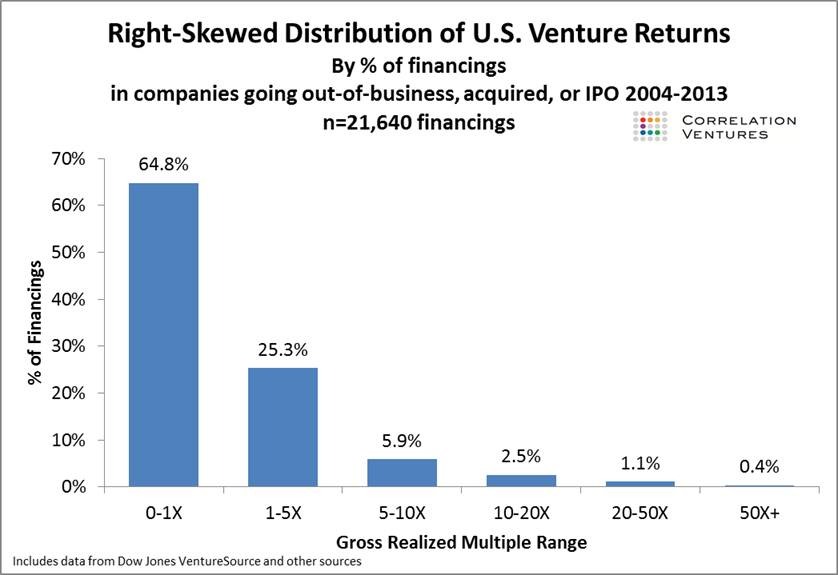

Based on Correlation Ventures data from 2004 to 2013, the odds are worse:

- Almost 65% of financings fail to return 1.0x capital invested.

- Only 10% produce a return of 5.0x or more.

- Only 4% produce a return of 10.0x or more.

Seth Levine actually ran the analysis for someone trying to return a $100M venture fund based on these averages (let’s hypothetically imagine it’s Bryant Stibel… just for arguments sake).

I’ll paraphrase Seth’s analysis but urge you to check it out yourself:

Per his calculations, a $100M fund with 20 companies would produce a gross return of $206M (before fees and expenses) which has an IRR around 10%.

The more important thing here is the challenge of finding companies at the right side of the distribution chart . In this $100M fund with 20 investments, the total number of financings producing a return above 5x was 0.8 — producing almost $100M of proceeds. Seth’s theoretical fund didn’t find its ‘purple unicorn’, just 4/5ths of that company. If they had missed it, they would have failed to return the funds investment, net of fees.

{kind=link}

CB Insights even went as far as to narrow the return criteria by stage and round. Maybe the fund’s dynamic or willingness to take losses changes when you are investing your own earnings instead of your LPs. It’s just hard to make outsized returns in the venture game and by many accounts it’s getting even harder.

There is a ton of money floating around startups today, whether from super angels, micro VCs, corporate VC arms or giant mutual funds and the “sure-thing” rounds at later stages are getting more and more crowded with sharper elbows and liquidation preference stacks meaning you can lose much of the benefit of getting into a given round at a lower valuation.

Plus if you thought restaurants are bad and illiquid investments with long return horizons, most startups are even worse. There has been a notable lack of exits for venture backed companies over the last few years — perhaps due to the relative ease of access to and cheapness of private capital from the sources listed above, or perhaps because founders don’t trust their fate in the public markets. But in either case, lack of liquidity continues to be a problem for many VCs and even if many of early-stage funds look good on paper, their “paper returns” won’t mean anything until the companies actually exit.

Ask the investors of Fab, GILT, Mindbody, DraftKings or Square how great these investments once looked on paper.

Last Stop on The Gravy Train

So what do you do if you’re a newly retired athlete or a current one coming close to hanging up the cleats. Your last contract is burning a hole in your pocket and you’ve got a real desire to forge a new career in the ‘hot new’ technology sector. I’ve actually got a few thoughts for you:

Don’t just invest in startups. Go start one yourself!

The world could always use more founders. More passionate, driven people with unique ideas willing to take a chance on themselves and build something from nothing. That doesn’t mean be frivolous with your capital — it means bring the same dedication, diligence and hustle you put into your craft on the court or field to building a product people will love. That creates actual value.

As an athlete and celebrity, you have the financial security to experiment, iterate and launch new products faster and with better resources than most first-time founders. Use that to your advantage. Go build the next Player’s Tribune or Slyce or Uninterrupted.

Become a student of the game. Go work for a startup.

Patrick Willis leveraged his time as an athlete in Silicon Valley to build connections and scout opportunities, joining Open Source Storage after retiring. One of the greatest linebackers in modern NFL history, Willis terrorized the line of scrimmage and earned Pro Bowl honors in seven of his eight professional seasons. Now he spends his days focused on building strategic partnerships in the media and entertainment sectors for a venture-backed company. His new game is crushing sales calls and closing deals.

This isn’t about squashing your ego and trading in the huddle for a cubicle, nor do many athletes need the day-job for the paycheck. Willis is a great model for someone that wants to make a smooth transition from player to technology professional. I think many athletes have extensive interpersonal skills to help them achieve success in sales, business development, communications or operations. Likewise, working in small teams, in a face-paced, constantly changing environment will offer both an easier transition into retired athlete life as well as a crash course in how to build and manage a growing company.

If you’re dead set on being a VC, be hands on and add real value

The smart entrepreneur doesn’t just need an investor just for their money. They want to align with people that share their vision and will be active partners in the process. Depending on the stage, those needs ranges from helping secure partnership deals, launching new markets, hiring new executives, product feedback, helping secure follow-on funding or advising on potential M&A.

While useful as an initial marketing push, the least valuable thing an athlete investor can offer is an endorsement. Even Kobe and Melo’s funds make that clear:

“We don’t want to be in the business of investing in companies so someone can use Kobe as an endorser. That’s not interesting,” Stibel told the Wall Street Journal.

Melo 7 Tech’s Goldfarb told TechCrunch that while he’s happy to take advantage of Anthony’s celebrity contacts, “help is never, ever in terms a commercial endorsement from Carmelo Anthony”.

Kobe Bryant isn’t the first athlete investor and unfortunately, I don’t think he will be the last. The higher profile and more prolific the investor, the greater the demands on his or her time will be and the lower likelihood they will consistently be really able to add value in each of their companies. In this way, even the most well meaning athlete can become disengaged over time, further perpetuating the stereotype that celebrities are dead weight on the cap table.

Athletes should understand that some of the value-add will come more easily than others but the most successful of these ‘athlete investors’ will aim to be more of the latter and less of the former over time.

In Conclusion: You Can’t Eat Preferred Stock

I suppose it all comes down to why athletes and celebrities want to be involved with startups in the first place.

My guess is that for some, it really is about the passion for technology and media innovation and their ability to translate that passion into becoming the ultimate early-adopter. For others, I think it’s about discovering a second career and venture capital is one where they don’t have the same barriers to entry — they can self fund instead of having to raise funding from LPs. The smartest among them will partner with someone who has had tangible experience and success as a venture investor. While I can nitpick at motivations, having more excited and diligent investors with capital to invest in new technology is overall a good thing for startups.

What worries me are the wrong lessons I feel prospective athlete investors will take from Kobe’s or Andre’s or Peyton’s success. Just because you have money, doesn’t mean you will inherently be good at identifying startups for investment. The profiles of most early stage funds overwhelmingly expect one or two investments to cover the entire fund, meaning that if you happen to miss that one investment, you wouldn’t even make a return. Add to that the lack of large exits, whether by M&A or IPO and consider whether you can truly afford to wait 5–7 years for a given investment to bear any fruit. In the face of these overwhelming odds, I caution any “me-too” athlete investors.

Bad investments are the cornerstone of the retired professional athlete’s riches-to-rags story but at least when your steakhouse is failing, you can head over to the kitchen for a warm meal.

My thanks to Samir Chainani and Danny Crichton for indulging my ideas on this topic over the course of putting together this article and Correlation Ventures and Seth Levine for their data.